Understanding Working Capital Finance for Consumer Brands

Introduction

Consumer brands—especially those manufacturing physical goods—regularly face a cash flow challenge. They often pay for inventory months before receiving the cash from customers. Once the product is manufactured, shipped, sold, and payment is collected, the lag can span 3–9 months, creating a working capital gap.

Working capital financing bridges this gap. It allows brands to fund inventory, marketing, and operations today using the confidence of future cash inflows. Below is a linear progression of working capital solutions, from seed-stage startups to enterprise-level operators.

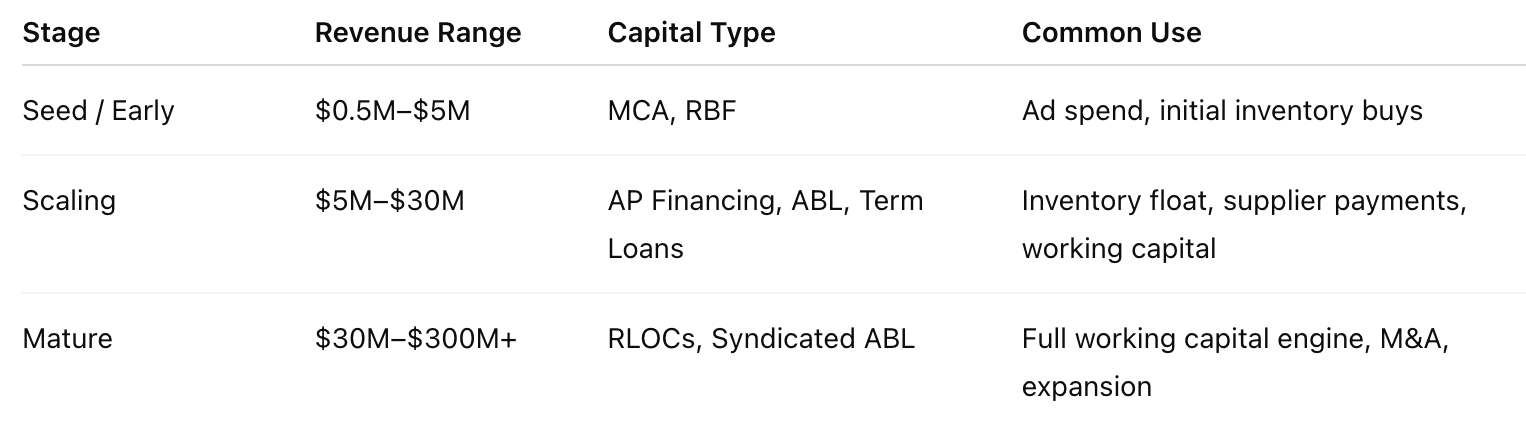

1. Early-Stage Solutions ($500K–$5M Revenue)

At this stage, brands often can’t access traditional credit lines. They rely instead on revenue-based or merchant-style advances that are fast, automated, and linked to sales performance.

Shopify Capital / Merchant Cash Advances

Short-term advances repaid via a fixed % of daily Shopify sales.

Pros: Fully automated, no credit checks or personal guarantees.

Cons: High effective APRs; repayments can strain cash flow during slow seasons.

Performance-Based Cash Advance Lending

Capital advances against projected sales or ad performance (e.g., Meta, Google).

Pros: Quick access, no equity dilution.

Cons: High repayment rates; capital limits tied to historical sales.

Accounts Payable (AP) Financing

Providers like Settle pay your supplier upfront; you repay in 30–90 days.

Best for: Extending payment terms with overseas or rigid suppliers.

Pros: Tailored to CPG/DTC workflows; integrates with accounting tools.

Cons: Short-term, non-revolving structure.

💡 Emerging trend: Many early-stage lenders now use AI and revenue data integrations (Shopify, Amazon, Meta) to automate underwriting and optimize cash flow forecasting.

2. Growth-Stage Credit Facilities ($5M–$30M Revenue)

As brands scale, they become eligible for structured credit such as term loans and revolving lines of credit (RLOCs) backed by inventory and accounts receivable.

Revolving Line of Credit (Asset-Based)

Borrowing base: ~85% of A/R and 50–65% of finished goods.

Pros: Scales with growth; interest-only periods; well-suited for DTC models.

Cons: Reporting requirements; financial covenants; slower to deploy than merchant advances.

Hybrid RLOC + Term Loan Facilities

Offers both term loans and revolvers, often with flexible sub-limits (e.g., higher advance rates for Amazon or retail POs).

Pros: Designed for consumer brands; customizable draw schedules.

Cons: Requires diligence; may include closing and monitoring fees.

💡 Note: Many mid-market lenders now embed inventory visibility tools and sales analytics to dynamically adjust borrowing bases and improve working capital efficiency.

3. Institutional Bank Financing ($30M–$300M+ Revenue)

At this stage, brands with proven performance and clean books can access institutional bank credit—customized asset-based lending (ABL), revolvers, or syndicated credit lines.

Facility sizes range from $10M–$100M+.

Revolvers tied to A/R, inventory, and sometimes retail POs or Amazon receivables.

Pros:

Lower interest rates (Prime + 1–2%).

Deep treasury integration (FX, cash sweeps, wire automation).

Credibility with investors and vendors.

Cons:

Heavy diligence and field exams.

Strict covenants (FCCR, current ratio, liquidity floors).

Borrowing base reduced by ineligible assets (aged A/R, WIP inventory).

💡 Trend: Institutional lenders increasingly integrate ERP and supply chain data to automate borrowing base updates and reduce manual reporting.

4. The Core Principle of Working Capital Finance

Regardless of stage, the principle remains the same:

You pay for inventory, packaging, and freight today—but don’t get paid until months later.

Example timeline:

Day 0: Pay $300K to supplier in China.

Day 60: Product arrives in the U.S.

Day 90–120: Product sold and delivered.

Day 150–180: Cash collected (Amazon, Net-30 wholesale, etc.).

Without financing: You front 100% of the cost.

With working capital tools: You pay over time, aligned with your revenue cycle.

5. Financing Progression by Revenue Stage

Conclusion: From Ad-Based Advances to Institutional Credit

Working capital finance is not one-size-fits-all. The smartest brands build a credit ladder—starting with merchant advances, evolving into structured debt facilities, and eventually graduating to full-scale bank partnerships.

This evolution allows founders to:

Grow without excessive equity dilution.

Avoid cash-flow bottlenecks.

Align repayment with real revenue cycles.

Build institutional readiness for long-term scale.

The most sophisticated operators view working capital not as a burden—but as a strategic growth tool.